News Analysis

Case Study

Why So Many Digital Modernization Efforts Stall

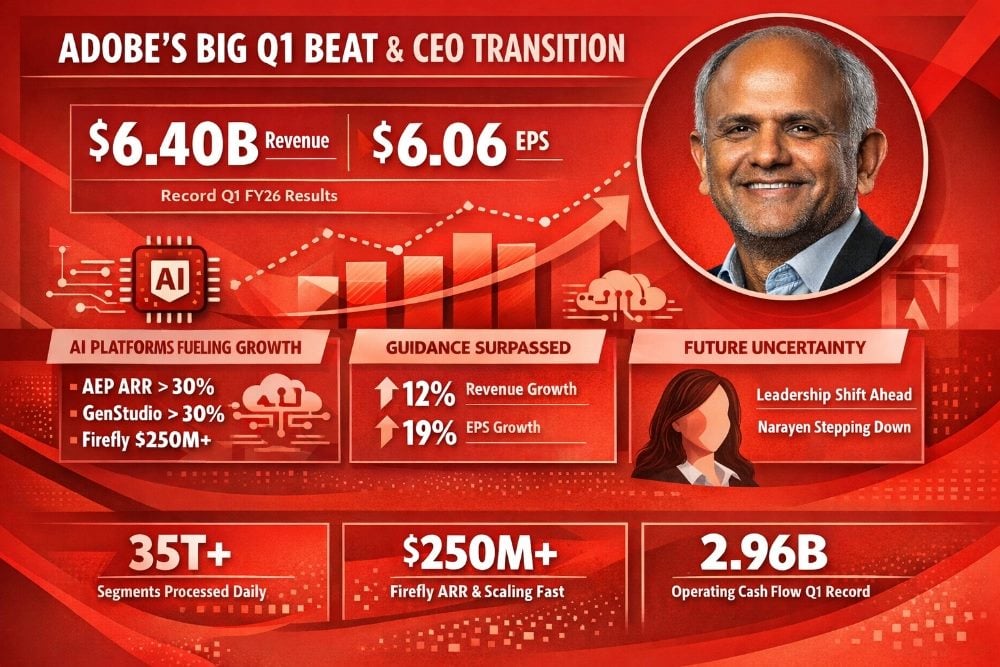

Adobe reported record Q1 fiscal year 2026 results on March 12 — the same day it announced that Shantanu Narayen, its CEO of 18 years, will step down once a successor is named. The dual announcement dominated headlines, but for digital experience practitioners, marketing technology leaders and enterprise teams running Adobe's stack, the earnings tell a story that deserves its own careful read.

Total revenue hit $6.40 billion for the quarter, up 12% year-over-year, beating the high end of guidance Adobe had set just one quarter earlier by roughly $100 to $150 million. Non-GAAP EPS came in at $6.06, up 19% year-over-year and well above the $5.85 to $5.90 guidance range. Record Q1 operating cash flow reached $2.96 billion. By nearly every measure, Adobe's business is performing ahead of its own expectations at the start of what is shaping up to be a pivotal year.

But the headline numbers only get you so far. What matters to practitioners, architects and digital leaders whose daily work runs on Adobe Experience Manager, Adobe Experience Platform, GenStudio and the broader Customer Experience Orchestration stack — is where the growth is actually coming from, what it signals about product roadmap continuity and what questions the Narayen succession opens up for the enterprise Digital Experience Platform (DXP) market.

On Dec. 10 Adobe set its Q1 FY26 targets publicly. Three months later, it beat every one of them. This is not a minor footnote — at Adobe's scale, outperforming the top end of revenue guidance by more than $100 million in a single quarter reflects genuine demand strength, not accounting timing.

Adobe set these targets in December 2025. The Q1 FY26 actuals show a broad-based beat across every major metric — particularly notable for the Creative and Marketing Professionals segment, which houses Adobe Experience Manager (AEM), Adobe Experience Platform (AEP), and GenStudio.

| Metric | December Guidance Low | December Guidance High | Q1 FY26 Actual |

|---|---|---|---|

| Total Revenue | $6.25B | $6.30B | $6.40B |

| Creative & Marketing Professionals Subscription Revenue | $4.30B | $4.33B | $4.39B |

| Business Professionals & Consumers Subscription Revenue | $1.74B | $1.76B | $1.78B |

| Non-GAAP EPS | $5.85 | $5.90 | $6.06 |

| GAAP EPS | $4.55 | $4.60 | $4.60 |

These full-year targets, set in December 2025 and reaffirmed after Q1, are the financial framework Adobe's digital experience business is being measured against for the year. Targets exclude the pending Semrush acquisition.

| Metric | FY26 Target | FY25 Actual | Context |

|---|---|---|---|

| Total Revenue | $25.90B – $26.10B | $23.77B | ~9–10% growth |

| Total Adobe ARR Growth | 10.2% YoY | 11.5% YoY | Highest net new ARR guide ever (~$2.6B) |

| Creative & Marketing Professionals Subscription | $17.75B – $17.90B | N/A (new segmentation) | Includes AEM, AEP, GenStudio, Firefly Enterprise |

| Non-GAAP EPS | $23.30 – $23.50 | $20.94 | ~12% growth |

| Non-GAAP Operating Margin | ~45.0% | ~45.0% | Sustained at scale through AI investment cycle |

Editor’s note: Key questions practitioners and enterprise digital leaders may have after Adobe’s Q1 FY26 results, leadership transition announcement and accelerating AI-driven platform growth.

Anil Chakravarthy, president of Adobe's Customer Experience Orchestration Business — notably rebranded from "Digital Experience" since the December earnings call, a deliberate repositioning that signals Adobe's intent to own the orchestration narrative — delivered the metrics that matter most to practitioners running Adobe's enterprise stack.

Adobe Experience Platform and native apps ending ARR grew over 30% year-over-year in Q1 FY26. GenStudio ending ARR grew over 30% year-over-year. Firefly ending ARR across the Firefly app, credit packs, and Firefly Enterprise exceeded $250 million — the first time Adobe has given a standalone ARR figure for Firefly as a business. Total customers with ARR over $10 million grew more than 20% year-over-year. And 70% of all AEP customers are now actively using agentic capabilities — not in pilot, but in production.

The platform scale metrics reinforce the enterprise-grade infrastructure story. AEP is now processing over 35 trillion segment evaluations and more than 70 billion profile activations per day. During the 2026 Super Bowl, Adobe-enabled experiences peaked at more than 8 billion analytics server hits, 21 million concurrent viewers, 34 million page views and 216 million emails delivered.

These are the metrics most directly relevant to enterprise teams running Adobe's digital experience stack, spanning the platform, content supply chain, and brand visibility pillars of Adobe's CXO business.

| Product / Capability | Q1 FY26 Metric | Prior Period Benchmark | What It Signals |

|---|---|---|---|

| AEP and Native Apps Ending ARR | Over 30% YoY growth | Over 40% YoY in Q4 FY25 | Moderation at scale; still strong absolute growth |

| GenStudio Ending ARR | Over 30% YoY growth | Over 25% YoY in Q4 FY25 | Accelerating — content supply chain gaining committed spend |

| Firefly Ending ARR (app + credit packs + Enterprise) | Exceeded $250M | First public Firefly ARR figure | Firefly now a standalone ARR business at meaningful scale |

| AEP Agentic Capability Adoption | 70% of all AEP customers | N/A | Production adoption, not pilot experimentation |

| Customers with ARR Over $10M | Over 20% YoY growth | Over 25% YoY in Q4 FY25; over 150 total | Wallet share expansion among largest enterprise accounts |

| Agentic Web Trials (LLM Optimizer, Sites Optimizer, Brand Concierge) | 650+ active customer trials | 50+ customers in Q4 FY25 | Strong sequential pipeline acceleration |

| Firefly Enterprise New Customer Acquisition | 50% YoY growth | Over 100 new deals in Q4 FY25 | Enterprise content automation demand accelerating |

| Custom Firefly Models via Foundry | Over 2,500 since launch | Announced at Adobe MAX, October 2025 | Brand-specific AI model adoption scaling across verticals |

| Generative Credit Consumption | Over 45% growth QoQ | 3x QoQ growth in Q4 FY25 | Leading monetization indicator for AI upsell and ARR expansion |

It is worth being precise for readers tracking the trajectory. AEP and native apps ending ARR grew over 40% year-over-year in Q4 FY25, then over 30% in Q1 FY26. That is a deceleration, and at Adobe's scale it is not alarming, but it is real and worth noting honestly. GenStudio moved in the opposite direction: from over 25% in Q4 FY25 to over 30% in Q1 FY26. That acceleration suggests the content supply chain platform is gaining committed enterprise spend as the AI-powered content production use case matures from concept to production workflow.

For AEM customers, the most strategically significant section of Q1 earnings was Chakravarthy's framing of the agentic web opportunity. The argument Adobe is making is direct: as consumers increasingly discover brands and make purchase decisions through LLMs and AI agents rather than traditional search, the stakes around brand visibility have fundamentally changed — and AEM sits at the center of Adobe's answer to that shift.

Adobe's own Digital Insights data, drawn from more than one trillion visits to U.S. retail sites during the 2025 holiday season, showed LLM-driven traffic growing nearly sevenfold year-over-year. More importantly, Adobe found that LLM-referred traffic converts 31% higher and generates 254% more revenue per visit than traditional referral traffic. That is a commercial argument for why AEM, LLM Optimizer, Sites Optimizer and Brand Concierge are not incremental add-ons — they are the enterprise's answer to a structural shift in how customers find and engage with brands online.

As of Q1, over 650 customer trials are underway for Adobe's agentic web product suite, up from just over 50 at the end of Q4 FY25. The pending Semrush acquisition — a $1.9 billion all-cash deal expected to close in Q2 — is positioned to complete this picture by adding search engine optimization and generative engine optimization capabilities that extend Adobe's brand visibility solution from owned web properties into traditional search and LLM environments simultaneously.

Related Article: AEO, GEO, SEO: What's the Best Search Playbook?

GenStudio's Q1 story goes beyond ARR growth. A capability highlighted in the Q1 prepared remarks matters significantly for enterprise marketing operations teams: GenStudio-created assets can now flow directly into activation workflows across the Adobe stack and into paid media platforms including Amazon Ads, Google, LinkedIn and Meta. That closed loop — from ideation and creation inside GenStudio to paid media activation and analytics measurement — is the operational reality Narayen described on the Q4 FY25 call as Adobe being "the only company that can close the loop from the creation of a campaign, the execution of that campaign as well as then actually looking at what that causes in terms of commerce."

On the Q4 FY25 call, David Wadhwani, president of the Creativity & Productivity Business for Adobe, offered the most concrete enterprise economics example to date for Firefly Foundry. A media and entertainment company spending $10 million ARR on core Adobe creative products was upsold Firefly Services and Foundry for an additional $7 million — a 70% step-up in spend — with custom models trained within two to three months and already driving revenue-bearing content production integrated with Adobe's real-time Customer Data Platform (CDP).

Narayen's vision is explicit: a custom Foundry for every brand, every franchise, every TV show or film. With over 2,500 custom Firefly models now built since launch, that vision is moving from aspiration to operating reality.

Firefly Enterprise new customer acquisition grew 50% year-over-year in Q1. Generative credit consumption grew more than 45% quarter-over-quarter, with video generative actions growing more than eight times year-over-year and audio generative actions doubling. Those consumption metrics matter because generative credits are how Adobe monetizes AI usage across its creative and marketing professional base — and accelerating credit consumption is the leading indicator for upsell and ARR expansion in the quarters ahead.

Adobe's Q4 FY25 results, reported in December 2025, established the baseline from which Q1 FY26 should be read. Digital Experience segment revenue for the full year reached a record $5.86 billion, up 9% year-over-year. Digital Experience subscription revenue hit $5.41 billion, up 11%. AI-influenced ARR, broadly defined, exceeded one-third of Adobe's entire book of business by the end of Q4.

These figures from the Q4 FY25 earnings call provide the baseline against which Q1 FY26 Customer Experience Orchestration performance should be measured. The segment was rebranded from Digital Experience to Customer Experience Orchestration at the Q1 FY26 call.

| Metric | FY25 Full Year | YoY Growth | Significance for DXP Practitioners |

|---|---|---|---|

| Digital Experience Segment Revenue | $5.86B (record) | 9% YoY | Anchors AEM, AEP, GenStudio, Analytics enterprise spend |

| Digital Experience Subscription Revenue | $5.41B | 11% YoY | Subscription growth outpacing total segment — recurring base expanding |

| AEP and Native Apps Ending ARR | N/A | Over 40% YoY in Q4 | Fastest-growing platform component entering FY26 |

| GenStudio Ending ARR | N/A | Over 25% YoY in Q4 | Content supply chain gaining enterprise budget share |

| Firefly Services and Foundry ARR | N/A | More than doubled YoY in Q4 | Content automation hitting enterprise deployment scale |

| Customers with ARR Over $10M | Over 150 total | 25% YoY growth in Q4 | Record number of large enterprise accounts added in Q4 |

| AI-Influenced ARR Share | Over one-third of total book | Accelerated throughout year | AI now embedded as a growth driver across the full business |

We examined what the December numbers suggested about AI's role in driving Digital Experience growth versus broader infrastructure modernization. The analysis and the practitioner voices remain directly relevant to reading Q1 FY26.

Patrick Calder, marketing director at Distillery, offered a pointed observation that holds up quarter-over-quarter: "The signal that stands out in Adobe's Digital Experience (full-year) earnings is contract size growth, not adoption breadth. Orders from enterprise customers are growing as they implement AI in operations, but there's little to show new customer acquisition tied to the transformative potential of AI."

Calder's reading — that DX growth reflects deeper spend among existing enterprise accounts more than net-new AI-driven adoption — is consistent with Q1 FY26, where growth in customers with over $10 million in ARR tells a wallet share expansion story as much as a market penetration one.

Kaveh Vahdat, founder and president at RiseAngle, framed where AI is delivering the most tangible DX value: "In DX, the most tangible value tends to show up where AI reduces cycle time: producing compliant creative variations faster, turning customer data into usable audiences, and orchestrating journeys with less manual work."

That framing maps directly onto what GenStudio, Firefly Services and AEP's agentic capabilities are designed to deliver — and it explains why enterprises with strong data foundations are seeing faster returns than those still working through fragmented customer data infrastructure.

Steve Morris, founder and CEO at NEWMEDIA.COM, added a critical operational perspective on AI governance inside Adobe DX deployments: "To maximize AI ROI in Adobe Experience Platform, real governance is an ally of scale. As we put guardrails in place, our teams actually move faster."

Morris also flagged the ownership gap that AI-generated experiences create in production: AI can generate code and content, but it cannot take ownership of maintainability, accessibility, or security — a caution that enterprise AEM and AEP teams running at scale would do well to internalize before expanding agentic deployments.

Burkan Bur, managing director at The Ad Firm, offered the most structurally challenging read on the growth numbers: "While AI accounts for 35% of the growth of this shift, the remainder of the trend is simply based upon general cloud migrations."

Bur's point — that much of Adobe's DX revenue growth reflects the infrastructure modernization required to support AI rather than AI-driven decisioning itself — is worth sitting with carefully as Adobe makes the case to enterprise buyers that its AI investments translate directly into measurable marketing ROI.

Narayen's announcement that he will step down as CEO once a successor is identified landed on the same day as the Q1 results, making March 12 one of the most consequential single days in Adobe's recent history. The board has appointed Lead Independent Director Frank Calderoni to chair the special committee overseeing the search, which will consider both internal and external candidates. Narayen will remain as Chair of the Board.

For the enterprise DXP community, the succession question is not abstract. The product bets that define the AEM and AEP roadmaps — the push into agentic web, the GenStudio content supply chain vision, the Firefly Foundry enterprise model, the Semrush integration — were all made under Narayen's leadership. An incoming CEO who prioritizes differently, or who arrives from outside Adobe's culture of deeply integrated platform thinking, could alter the trajectory of investments that enterprise architects and digital experience teams are currently planning around.

When asked on the Q1 earnings call what the board is looking for in a successor, Narayen was characteristically forward-leaning: "At our core, we're always going to be a product company. And taking advantage of the immense opportunity that AI has across creativity and marketing is the real opportunity." The search is expected to take several months.

Related Article: Adobe CEO Shantanu Narayen to Step Down After 18 Years

These figures illustrate the scale of transformation Narayen oversaw at Adobe — from a packaged software company to one of the largest enterprise SaaS and digital experience platform businesses in the world.

| Metric | When Narayen Became CEO (2007) | Today |

|---|---|---|

| Annual Revenue | Under $1B | Over $25B |

| Employees | ~3,000 | Over 30,000 |

| Total Adobe ARR | N/A (pre-subscription model) | $26.06B exiting Q1 FY26 |

| Business Model | Packaged perpetual software | Cloud-first SaaS and enterprise DXP |

| Digital Experience Revenue | Nascent / pre-major acquisition | $5.86B annually (FY25 record) |

| AI-First ARR | N/A | Tripled year-over-year in Q1 FY26 |

| Earnings Calls as CEO | 0 | 100 (Q1 FY26 was his last) |

What Narayen leaves behind is a company that has grown from under $1 billion in revenue to over $25 billion, with a digital experience business generating nearly $6 billion annually and an AI-first ARR line that tripled year-over-year in Q1 FY26. By his own framing on the earnings call, that AI-first book of business should become Adobe's next billion-dollar business. The CEO who takes the reins will inherit both that opportunity and the execution pressure that comes with it.

On March 13, Adobe disclosed the resolution of its Department of Justice lawsuit, originally filed in June 2024, over subscription disclosure and cancellation practices. The settlement terms: $75 million in free services to qualifying customers, and a $75 million cash payment to the DOJ. Adobe denied any wrongdoing and emphasized that it has since made its sign-up and cancellation processes more streamlined and transparent.

For enterprise AEM and Experience Cloud buyers — who routinely negotiate multi-year, multi-seat agreements with complex terms — this settlement is relevant context. The DOJ case put a spotlight on how Adobe structures, discloses and allows exit from subscription commitments. Enterprise procurement leaders and legal teams negotiating Adobe contracts going forward would be well-served to ensure cancellation terms, auto-renewal clauses and pricing escalators are explicitly documented and agreed upon before signing.

For the record: the $62 million loss contingency that appeared in Adobe's Q1 FY26 non-GAAP reconciliation tables — unexplained in the press release itself — was this settlement. Adobe knew the resolution was coming when the quarter closed. It is now resolved and behind them.

Related Article: FTC Sues LA Fitness Over Membership Cancellation Barriers

CMSWire will be on site at Adobe Summit next month in Las Vegas. Chakravarthy closed his Q1 prepared remarks by pointing directly to Adobe Summit in April as the venue where significant new innovations and partnerships will be unveiled. For the digital experience community, Summit is where Adobe's product narrative gets translated into roadmap specifics, customer case studies and partner ecosystem announcements that practitioners can actually act on.

Based on the Q1 earnings signals, the areas most worth watching are the maturation of the agentic web product suite — LLM Optimizer, Sites Optimizer and Brand Concierge — where 650-plus trials need to convert into committed paid deployments; the Semrush integration roadmap if the acquisition closes as expected in Q2; GenStudio's expanding activation ecosystem and how Adobe is closing the loop from content creation to paid media performance measurement; any AEP agent orchestration announcements building on the six new agents released in Q4 FY25; and leadership signals around the CEO succession that will inevitably color every major product announcement on the Summit stage.

The bottom line on Q1 FY26 is this: Adobe's digital experience business beat expectations, its AI-first ARR is tripling, its agentic web pipeline is accelerating, and its content supply chain platform is gaining committed enterprise spend. The Narayen succession introduces genuine strategic uncertainty. But the numbers Adobe delivered on March 12 suggest that the platform momentum his tenure built is, for now, intact and moving forward.

Check out CMSWire's coverage of Adobe Summit over the years.

Scott Clark is a seasoned journalist based in Columbus, Ohio, who has made a name for himself covering the ever-evolving landscape of customer experience, marketing and technology. He has over 20 years of experience covering Information Technology and 27 years as a web developer. His coverage ranges across customer experience, AI, social media marketing, voice of customer, diversity & inclusion and more. Scott is a strong advocate for customer experience and corporate responsibility, bringing together statistics, facts, and insights from leading thought leaders to provide informative and thought-provoking articles. Connect with Scott Clark: